Earlier this month, the IRS provided guidance for employers claiming the employee retention tax credit for 2020.

Changes Under December 2020 Stimulus Plan

As detailed in a previous Gould & Ratner article on the extension and expansion of the employee retention tax credit, the stimulus bill passed by Congress at the end of 2020 retroactively amended the employee retention credit to allow eligible employers to claim the credit even if the employer obtained a Paycheck Protection Program (PPP) loan. Eligible employers may now claim the credit on any qualified wages that are not counted as payroll costs in obtaining PPP loan forgiveness.

Guidance for Employers Who Received a PPP Loan on Claiming Employee Retention Credit for 2020

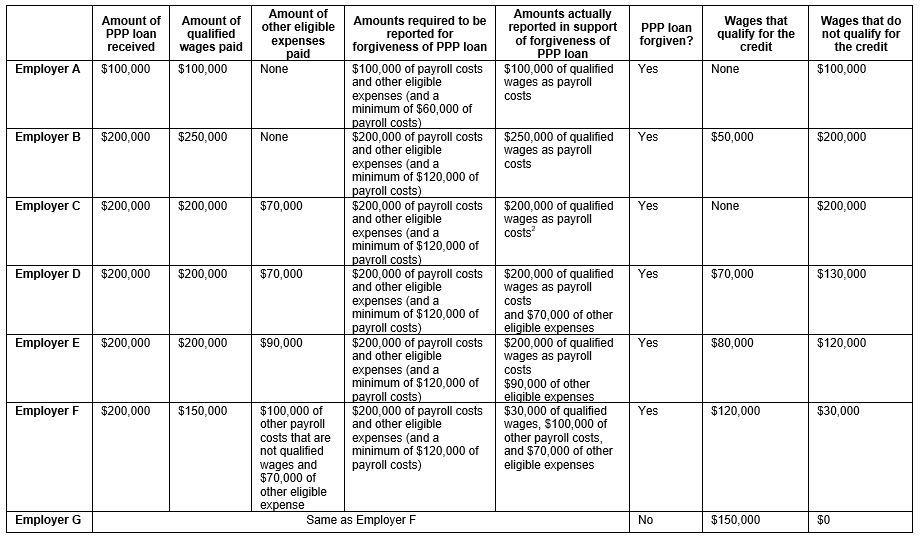

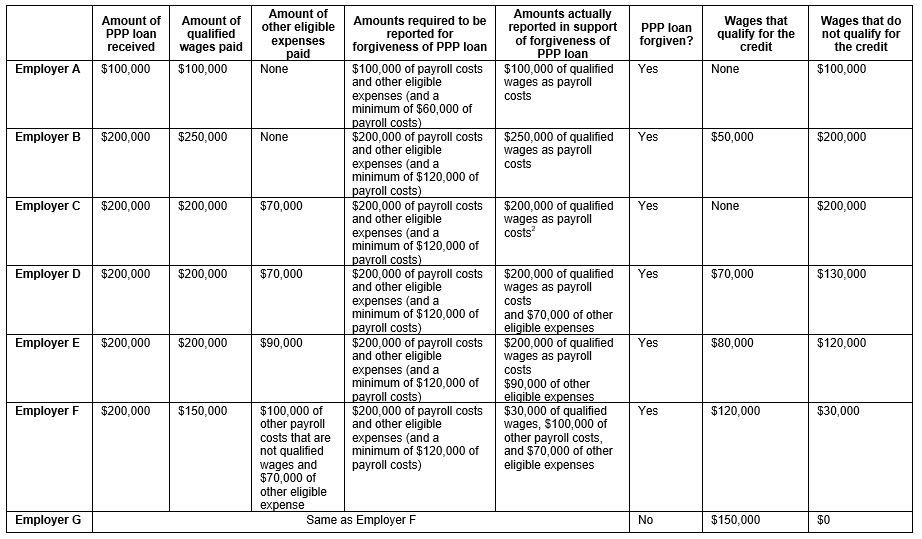

An eligible employer that received a PPP loan is deemed to have made an election not to take into account, for purposes of the credit, qualified wages included in the amount reported as payroll costs on a PPP loan forgiveness application. The credit does not apply to the qualified wages for which a deemed election is made. The below chart summarizes several examples set forth in the guidance that illustrate the interaction between PPP loans and the credit.1

The guidance issued this month addresses only the rules applicable to 2020. The IRS plans to release additional guidance addressing the changes for claiming the credit for 2021.

If you have questions about the interaction of the employee retention credit with PPP loans, please contact one of the attorneys in Gould & Ratner’s Tax Planning and Compliance Practice.

[1] All examples assume that the employer is an eligible employer and that wages paid would qualify for the credit during the second and third quarters of 2020.

[2] This example illustrates an error on Employer C’s part of not reporting the $70,000 of other eligible expenses in applying for forgiveness.